Be in the know of the latest news and updates about Overseas Filipino Bank (OFBank).

Overseas Filipino Bank: The capstone of six years of financial momentum

(Written by Chris Wright May 30, 2022 | Published on Euromoney ) The Duterte presidency had many problems, but it gave the Philippine central bank and finance ministry room to enact significant change in tax, digital reach, infrastructure and fiscal policy. OF Bank will be among its legacies. The Philippines has long owed a debt to its overseas foreign workers (OFWs). Even after the disruptions of the pandemic, overseas workers sent back $31.4 billion to the country in 2021, and the central bank expects a 4% rise in that number this year. From Singapore to Saudi to a thousand merchant ships around the globe, these workers routinely send home sums equivalent to around 9% of the Philippines’ GDP. “Historically, OFWs have played a significant role in fuelling the country’s economic growth,” says Leila Martin, chief executive of Overseas Filipino Bank. “Now they are significantly contributing to our efforts to respond to the global health and economic crisis brought about by the Covid-19 pandemic.” OF Bank is a new institution – or more accurately an old one in a new form – which represents one of the signature missions of the now-ending regime of president Rodrigo Duterte: Financial inclusion. “We are trying … to make digital banking more accessible, more palatable to the appetite of Filipinos who traditionally are not very much into digital banking” Leila Martin, Overseas Filipino Bank OF Bank was formed out of the Philippine Postal Savings Bank as a wholly owned subsidiary of Land Bank of the Philippines, which is a state institution historically focused on serving the needs of farmers and fishermen. With its transition, OF Bank becomes the first government digital-only branchless bank in the country, and has a mandate to provide financial products and services tailored to the needs of overseas Filipinos. And that is quite a need. OFWs have a more vital role to the Philippines than even the headline numbers would suggest, because pretty much all of those remittances – to parents, to spouses, to siblings, to kids – then go straight into productive use in the domestic economy. They are spent on food, housing, education and all the other things that domestic helpers, sailors and hospital workers around the world are sending money back to support. “These remittances elevate not only the financial conditions of their own families, but the financial position of the Philippines, spurring economic growth,” Martin says. Yet they are underserved in their offshore communities, sometimes cruelly so. People trying to send remittances home are stymied at every turn: draconian one-off fees, often applied to each remittance, so that someone trying to send a transfer apiece to mum, sister and daughter gets hit by the same fee three times. The list of hinderances continues: absurd foreign exchange rates; unrealistic minimums. In the first instance, OF Bank is about making this easier. Workers can access OF Bank through an app with a few pieces of ID and some links on their phones required for registration. There is no required opening deposit, no minimum balance requirement nor fear that an account will be closed for lack of funds coming in. There is 24/7 availability, no charges at all if transfers are between OF Bank accounts or to other Landbank accounts, and fees of P15 to P25 (between $0.29 and $0.47) to other commercial banks in the Philippines. Martin says the bank is not at this stage handling FX, but it has offered retail onshore dollar bonds issued by the Bureau of the Treasury, and there are plans to tie up with other partners who ought to be able to trigger reductions in conversion rates. Up and running About 18 months into its existence as OF Bank, most of the key services are up and running; there are 75,000 retail accounts on board, and in the three months to April there were P1.8 billion in banking inflows, P800 million from the remittances base. There is also a broader point about digital banking as a mechanism for financial inclusion, which has been a mainstay of Duterte policy, or rather a mainstay of Bangko Sentral ng Pilipinas governor Benjamin Diokno and Finance Secretary Carlos Dominguez under the broader poverty alleviation ideas of the president. “What we are trying to do at OF Bank is to make digital banking more accessible, more palatable to the appetite of Filipinos who traditionally are not very much into digital banking because of the apprehension that money will be lost because it’s in the air,” Martin says. “The pandemic jump-started the reduction in the digital divide.” This is certainly true: Diokno has said many times how the pandemic, as a mechanism for forcing digital engagement, accelerated state ambitions in this area by years. In this respect, OF Bank’s ownership is important. It is certainly not the only digital bank underway in the Philippines: Euromoney has written before about Tonik, for example, and there are digital platforms backed by Union Bank, RCBC, EastWest, CIMB and ING, among others. But OF Bank is owned by a state institution whose entire mandate is to stand for the 'little guy'.\ “There is definitely a stability in being a government bank,” says Martin. “It assures people that their hard-earned money is safe and secure. It also brings the resources of the parent: Martin, a specialist in electronic and internet banking as well as project management, is one of many who was seconded to Land Bank to build OF Bank. “I know that at Land Bank, our success rests largely on [the] strategic direction set by the seniors and the protocols that were established and proven to be effective,” she says. “And that is basically the blueprint for OF Bank transitioning.” It also places OF Bank squarely within the context of the Duterte administration’s ambitions as that reign comes to an end. “We fulfilled president Duterte’s promise of establishing a bank dedicated to the needs of Filipino workers working abroad… our first branchless digital-only bank in the country,” said Dominguez at an event in Manila in April. “It now serves overseas Filipinos in 116 countries.” Credit That conference felt like old times: The great and the good gathered in the Reception Hall, PICC Pasay City, to see presentations from the ministry of fnance and the central bank, not on a screen but in person. Duterte’s time was coming to an end – the new president, Ferdinand 'Bongbong' Marcos, formally takes o?ce on June 30 – and there was a sense of n de siècle about it all, a setting out of achievements and a call for continuity from the successors to come. It is an interesting and uncomfortable contradiction that while the Duterte regime has been lamentable in human rights and freedom of speech terms, it has been strikingly successful in terms of financial policy. Most people in financial services tend to lay the credit for this at the door of Diokno and Dominguez rather than the president, but he does deserve credit for leaving them to do what they are good at. It is quite a list. Diokno calls it “six years of institutionalized game-changing reforms and shaping the economy.” Dominguez claims: “Years from now, when we bring down poverty to single digits, we will look back at this time as when we made the turn.” Let’s take each in turn. From the BSP’s perspective, reform under the Duterte term began with the formation of the interest-rate corridor framework in 2016. In 2017 came the National Retail Payment system, allowing interoperability among payment service providers. Then came amendments to the BSP Charter in 2019, enabling the central bank to issue its own debt securities, providing it with an additional instrument for managing financial system liquidity. The Covid emergency prompted the Financial Institutions Strategic Transfer Act, or Fist, a pre-emptive strike against non-performing loans as the pandemic kicked in. In fact, Covid would give Diokno the ammunition he needed to make further sweeping changes. “The Covid-19 pandemic did not deter us from pursuing game changing reforms,” Diokno said at the Pasay City event. “In fact, the pandemic proved to be a catalyst that accelerated many of our reforms such as digitization and sustainability in our financial system.” This could be seen in action in two signature BSP initiatives. One is the Digital Payments Transformation Roadmap 2020-23. This has a target to convert half of the total volume of retail payments into digital form and onboard 70% of Filipino adults into the formal financial system using payment or transaction accounts by 2023. The other is the Digital Banking Framework, a key part of the DPTR, which granted digital bank licences to six financial institutions by the end of 2021. “The issuance of the Digital Banking Framework also aims to advance financial inclusion and the adoption and growth of digital financial services in the country,” Diokno says. Other initiatives include enabling regulations on Islamic banks, in order to attract funds from Islamic investors, and aiming to channel funds into infrastructure requirements in the Bangsamoro Autonomous Region in Muslim Mindanao. There has been the introduction of the basic deposit account framework; as of the second quarter of 2021, the number of basic deposit account holders in the country reached 7.4 million. Some 90.5 million Filipinos have basic and other types of deposit accounts. And the Sustainable Central Banking Programme and other sustainability and ESG frameworks have been launched. “The reforms that we have instituted are the result of our openness to embrace new things and our courage to deal with the challenges of our times,” Diokno said at the end of his presentation. “The past six years bested our resilience as a nation. But we are emerging better and stronger because we opted to build windmills that have harnessed the winds of opportunity. “When the winds of change blow, some people build walls. Others build windmills.” Policy pay-offs That’s the central bank. How about the government? In terms of policy, two things stand out: Duterte’s signature Build Build Build programme, and tax collection reform. Build Build Build committed to raise infrastructure spending to above 5% of GDP – it should reach 5.9% this year, according to finance secretary Dominguez. The difference is most visible in the railways. The government says the railway system covered just 77 kilometres before Duterte took office and now stands at 1,209km; the number of operational stations (61) has risen to 208; while the 224 operational cars of 2016 have become 1,368 today. All told, the department of finance has agreed 28 concessional loan agreements for its ?agship infrastructure projects, including the Metro Manila Subway project. That has been a long time coming: the Philippines is thought to be the world’s most populous city without a mass transit system, and Dominguez is particularly proud of that one. “What had once been considered a dream subway is now about to become a reality,” he says, adding that “our ?scal discipline” is what made it possible to agree the concessional loan arrangements that got it going. In truth, not as much infrastructure has been brought to operational status as the government would have hoped. But latitude has to be given for the disruption caused by the pandemic. The tax side involves the Comprehensive Tax Reform Programme, which lowered taxes, both personal and corporate, while simultaneously expanding the base, incentives and collection skills. Dominguez appears prouder of tax reform than anything else. “The administration decisively passed and implemented the most comprehensive tax reform programme ever in this country,” he said in his presentation. “This provided robust and recurring revenues that help expand social services and support our massive economic investments in modern infrastructure.” It is easy to illustrate the progress that has been made on tax. The government has doubled the annual collection it takes from government-owned or controlled corporations, an average of P68.7 billion annually since Duterte took office. Also 99.5% of income tax returns are now filed online, compared with just 10% in 2015. Overall tax revenue has increased from 15.1% in 2015 to 16.1% in 2019, before Covid kicked in. The government says the various elements of tax reform raised P504.6 billion in incremental revenues during the first four years of implementation. Two other important initiatives were the so-called sin taxes – more formally a number of excise taxes on sweetened beverages, from which the government collects P104 million a day now, to improve funding for its universal health care programme – and the Rice Tarification Law, which lowered rice prices and, the government says, provided a flow of funds for the modernization of the agriculture sector. Taxes on other suitably sinful items, such as alcohol, tobacco and vaping products, have gone up three times since Duterte took power. The rice law should not be glossed over: Dominguez notes that it took 30 years of failed attempts before it came into being, opening up the Philippine rice market and – Dominguez says –removing rice as a contributor to the main inflation rate and instead lowering the price of a vital staple food for 100 million Filipinos. That is a stark reversal in fiscal terms. Prior to the law passing in 2019, the National Food Authority received an average of P11 billion a year in tax subsidies from 2005 to 2018, the government says. It has instead earned P46.6 billion in rice-import tariffs during the first three years of the law’s implementation. “The rice tarification law ensures that farmers benefit directly by providing at least P10 billion each year for mechanization, high-quality seeds, access to credit and training,” Dominguez says. Three other things have worked in the finance secretary’s credit: the Ease of Doing Business Act; the Philippine Identification Act, which the Land Bank of the Philippines says has cleared the way for 7.7 million formerly unbanked registrants to be part of the formal banking system through implementing – 61.3 million individuals have registered for the national identity system as of March 23; and the revival of the Reit Act. The capitalization of the real estate investment trust sector was now P269.7 billion in April. OF Bank should be seen in the context of all of these reforms. Indeed, so should its parent: Dominguez says the government has infused more capital into the Land Bank of the Philippines (and Development Bank of the Philippines) than all other administrations put together. He wants to change its image. “Land Bank’s image as a big rural bank is far in the rearview mirror,” he says. “The robust capital infusion reinforced Land Bank’s financial strength and allowed it to be an effective partner of the government in advancing its development agenda. The capital is being prudently managed and used to finance projects that are needed by the country, not just in the agriculture sector,” including healthcare, education, power generation and distribution, water, transportation and housing, all led by the private sector. Covid costs There’s also room now to take a reckoning of the policies that were implemented in order to defend the country against Covid. Without question, the pandemic delayed progress. “Before Covid happened, the Philippines was in great shape: our debt-to-GDP ratio was only about 40%, our fiscal deficit to GDP was only about 3%,” says Alfred Dy, analyst at CLSA. “There was a lot of optimism. “But when Covid hit, the government had to step into the picture, to prop up the economy.” Debt to GDP has gone up to 60%, GDP has shrunk, and the fiscal deficit has risen to perhaps around 8%. “So, there’s some added leverage" says Dy, "but it’s something the government had to do.” The government argues that the impact of Covid would have been much worse without its measures. It was already bad – GDP fell 9.6% in 2020 – but would have been a 13.3% drop without reforms, Dominguez claims. All told, the government spent P3 trillion in direct response to Covid, equivalent to 15.6% of GDP, and ?nanced it by prioritizing domestic borrowings as well as seeking o?cial development assistance, and then the international capital markets. Vaccines were financed through a joint arrangement with the World Bank, the Asia Development Bank and the Asia Infrastructure Investment Bank. Now, some of those measures are being unwound. The government’s provisional advance arrangements with the central bank stood at P540 billion at its peak, now P300 billion, and will be paid o? by June 12, Dominguez says. Initial fears for the health of the banking sector so far appear overdone – although nobody is out of the woods yet, and the Fist Act, which for a while seemed a useful backstop that wasn’t going to be needed, may yet prove essential. “Because of the Covid crisis, you’ve seen non-performing loans moving up a bit,” Dy says. "But clearly what you’re seeing now can’t be compared to what we saw in the 1990s with the Asian financial crisis." “Because of the Covid crisis, you’ve seen non-performing loans moving up a bit,” Dy says. "But clearly what you’re seeing now can’t be compared to what we saw in the 1990s with the Asian ?nancial crisis." Then, system NPLs went as high as 20%; today they stand at 4.5%, and among the bigger banks that CLSA covers, below 3%. “The banks are well-capitalized, and the feeling on the ground is that if we are at 4.5% NPLs, that is quite good. We don’t see any systemic risk,” says Dy. CLSA is forecasting 7% to 8% loan growth this year, up from 4% to 5% last year. The Philippines underwent a multi-year push to hit investment-grade and its status has not yet been threatened by the pandemic. In February, Fitch a?rmed the Philippines as BBB, albeit with a negative outlook, citing strong external bu?ers and growth but weaker structural indicators including per capita income and governance. “The negative outlook reflects uncertainty about medium-term growth prospects as well as possible challenges in unwinding the policy response to the health crisis and bringing government debt on a firm downward path,” the agency says. It forecasts a recovery from 5.6% GDP growth in 2021 to 6.9% in 2022 and 7% in 2023. At Moody’s, Joyce Ong maintains a stable outlook for the Philippines banking system. “The accelerating in?ation due to the Russia-Ukraine military conclict, lingering pandemic woes due to new variants, and possible rate hikes in the country will dampen but not derail the economy’s recovery,” she says. She expects bank profitability to improve as provisions decrease and core earnings pick up. She also thinks banks recognized most of the defaults by pandemic-hit small and medium-sized enterprises and retail borrowers in 2021, and therefore expects NPL growth to slow through 2022. In the aggregate, Diokno and Dominguez can look back on their work under Duterte with some satisfaction. And when it looks back years from now, perhaps OF Bank will be among the signature achievements of the period: Finally giving a hard-working and essential part of the Philippine national identity the Financial services they deserve. “We want to further our portfolio,” says Martin, “with an ear to what the requirements are of our overseas Filipinos.”

VIEW ALL NEWS

OFBank becomes the first government digital-only and branchless bank; introduces new deposit products

The national government, spearheaded by the Department of Finance (DOF) and the Land Bank of the Philippines (LANDBANK), has launched the Overseas Filipino Bank (OFBank) as a digital-only, first branchless Philippine government bank that allows clients to complete banking transactions anytime and anywhere across the globe. The OFBank virtual launch today (June 29) was streamed live on the Facebook Pages of OFBank (@OFBank), and its parent bank, LANDBANK (@landbankofficial), and the LANDBANK YouTube Channel (/landbankofficial). The event was hosted online by TV personality Gretchen Ho. The virtual launch was made possible with the support of officials led by Finance Secretary Carlos G. Dominguez, OFBank Chair and LANDBANK President and CEO Cecilia C. Borromeo, OFBank President and CEO Leila C. Martin, Visa Country Manager for the Philippines and Guam Dan Wolbert, and the respective Board of Directors of OFBank and LANDBANK. “Despite the global health crisis besetting the country today, our government remains true to its commitment of upholding the welfare of all Filipinos abroad and their families. The launch of OFBank today as a digital-only, first branchless Philippine bank is a testament to this,” OFBank Chair Borromeo said. As a digital-only facility, the OFBank, a fully-owned subsidiary of LANDBANK, now utilizes Digital Onboarding System with Artificial Intelligence (DOBSAI) to facilitate real-time account opening via the OFBank’s Mobile Banking Application. The new digital account opening platform allows overseas Filipinos (OFs), overseas Filipino workers (OFWs) and their beneficiaries to securely and conveniently submit all requirements online. Opening an account using DOBSAI via the OFBank Mobile Banking App is safe and secure. The applicant will only need to take a “selfie” and the system will compare this photo with the photo in the valid identification (ID) card uploaded by the client. The app likewise has advanced encryption and security technology that protects sensitive information. There are three types of accounts available in OFBANK’s DOBSAI: the OFBank Visa Debit Card for OFs and OFWs, the OFBank Visa Debit Card for beneficiaries, and the OFBank Debit Card for beneficiaries below 18 years old. These are interest-bearing peso savings accounts with no minimum initial deposit and monthly average daily balance (ADB), as well as dormancy fee. To earn interest, the accounts need to have a daily balance of P500.00. The OFBank Visa Debit Card allows cardholders, specifically the beneficiaries of OFs and OFWs, to receive secure and convenient real-time fund transfers using Visa Direct, Visa’s real time payment solution through the 16-digit card number. “We’re extremely pleased to join our valued partner, OFBank in this launch to support OFWs, OFs and their beneficiaries. The reintroduction of OFBank as a digital-only, branchless Philippine bank is extremely timely when Filipinos are becoming more digital, and our research also shows that close to 80% of Filipinos are interested to use services from a digi-bank. We are glad to show our support to this community by enabling beneficiaries of OFWs and OFs to receive money in real-time by seamlessly and securely using the 16-digit OFBank Visa debit card, which they can also use to make face-to-face and online payments wherever Visa is accepted.” said Dan Wolbert, Visa Country Manager for the Philippines and Guam. OFBank account holders can use OFBank’s mobile facility to transfer funds to their beneficiaries’ OFBank and LANDBANK accounts, free of charge. Interbank fund transfers, on the other hand, are subject to a service fee of P25.00 per transaction via InstaPay and P15.00 per transaction via PesoNet. OFBank Online Channels The OFBank is also increasing its presence online to reach more Filipinos worldwide. In the virtual event today, the Bank likewise introduced its modified website – www.ofbank.com.ph. The newly redesigned site contains key information about OFBank, list of products and services, and answers on Frequently Asked Questions (FAQs) from the banking public, among others. As part of its efforts to be of greater service to its customers, the Bank also launched its official Facebook page – @OFBank. The OFBank believes that this is an effective tool to inform the public about the Bank’s latest developments and offerings since Facebook is one of the most used social media platforms by Filipinos across the world. The page will also be an additional channel through which client queries will be addressed. “As the OFBank becomes fully digital, we aim to better serve the banking and financing requirements of our kababayans abroad, as well as their families here in our country. Rest assured that OFBank will continuously work on providing safe, reliable and secure digital banking,” OFBank President and CEO Martin said.

LEARN MORE

OFBank launches online account opening platform with artificial intelligence

The Overseas Filipino Bank (OFBank) will be offering a new digital account opening platform supported by artificial intelligence when it is officially relaunched later this month as a fully digital, first branchless bank in the Philippines. Through the Digital Onboarding System with Artificial Intelligence (DOBS-AI), OFBank clients will be able to open a bank account in real-time at the convenience of using supported Android and iPhone devices. The platform utilizes artificial intelligence to facilitate an electronic know-your-customer (e-KYC) process to verify and validate uploaded application information and requirements. Clients can open OFBank Visa Debit Accounts designed for Overseas Filipinos and Overseas Filipino Workers, and an OFBank Debit Account for beneficiaries below 18 years old. By enrolling an OFBank Account in the OFBank Mobile Banking App, clients can transfer funds to OFBank and LANDBANK accounts free of charge, transfer funds to accounts in other banks via InstaPay or PesoNet, pay bills online to online merchants, pay cashless via Point-of-Sale (POS) terminals, and withdraw cash through local and international ATMs, among others. “OFBank’s transformation to a digital bank is geared towards servicing the evolving banking needs of migrant workers and Overseas Filipinos. By leveraging on technology, we have made it much easier to open an OFBank account and provide our clients convenient, secure, and responsive digital banking solutions,” OFBank President and CEO Leila C. Martin said. OFBank is a wholly-owned subsidiary of Land Bank of the Philipines (LANDBANK) mandated to provide financial products and services tailored to the requirements of Overseas Filipinos. LANDBANK President and CEO Cecilia C. Borromeo and OFBank President Leila Martin serve as the chairperson and vice chairperson of the OFBank Board of Directors, respectively. For more updates, please follow, like, and share the official LANDBANK social media accounts—for Facebook and Instagram: @landbankofficial, and for Twitter: @LBP_Official, and the LANDBANK website: www.landbank.com.

LEARN MORE

OFBank is officially first digital-only bank in PHL after obtaining BSP banking license

The Overseas Filipino Bank (OFBank) has officially become the first branchless digital-only bank in the country’s history after securing a digital banking license from the Monetary Board (MB) of the Bangko Sentral ng Pilipinas (BSP). A wholly owned subsidiary of the Land Bank of the Philippines (LANDBANK), the OFBank was able to commence its banking operations in June last year using its then existing license to operate as a thrift bank. The MB issued the OFBank’s digital banking license last March 25. Finance Secretary Carlos Dominguez III said “this milestone in the country’s banking history not only fulfills President Duterte’s campaign pledge to create a bank that caters to overseas Filipinos, but will also help the Philippines leapfrog to the digital economy.” “When President Duterte said he would create a bank that would serve overseas-based Filipinos, he wanted a bank that would be trailblazer in terms of modernizing and expanding the scope of the services it offers to them,” Dominguez said. “I commend the OFBank and the LANDBANK under its president-CEO Cecilia Borromeo for their tireless efforts that have led to the bank’s transformation into the Philippines first branchless and digital-only banking institution,” he added. The OFBank was created under Executive Order (EO) No. 44 that was signed by President Duterte in September 2017. To fulfill the EO’s provision on the “need to establish a policy bank dedicated to provide financial products and services tailored to the requirements of Overseas Filipinos (OFs), the Philippine Postal Savings Bank (PPSB) was acquired by LANDBANK and converted into the OFBank. On June 29 last year, the OFBank was launched virtually amid the COVID-19 pandemic as the Philippines’ first branchless and digital-centric government bank. While fine-tuning its operations, systems and processes to enable its official transition into a digital bank, the OFBank operated as a thrift bank. In December 2020, the BSP issued Circular No. 1105 on The Guidelines on the Establishment of Digital Banks, clearing the way for the OFBank to apply for a license as a digital bank. On January 20, 2021, the OFBank submitted a Letter of Intent to the Supervisory and Policy Research Department of the BSP signifying its interest to be a duly licensed Digital Bank and followed it up with an application last Feb. 1 for the conversion of its thrift bank license into a digital bank license. The OFBank offers four digital products and services that includes a Digital Onboarding System with Artificial Intelligence (DOBSAI), which allows the real-time opening of a mobile banking deposit account on supported iPhone or Android devices. As of December 2020, a total of 19,887 DOBSAI accounts in the OFBank have been opened with an outstanding balance of P104.37 million. Aside from deposit savings accounts, the OFBank’s digital services also includes fund transfers, bills payments and applications for multi-purpose loans. The volume of OFBank’s electronic banking inflows totalled 45,997 accounts as of December 2020 for transactions amounting to P467 million, with outflows from 62,633 accounts of P372.41 million. A total of 3,517 transactions amounting to P40.72 million were done by OFBank clients for the Premyo Bonds second offering and 380 transactions valued at P8.27 million for the RTB-25 (Retail Treasury Bond-25) issuance that were all coursed through the bank’s mobile application. The OFBank’s global digital reach spans 112 countries, with its clients able to access online the services of 763 merchants onboarded in its mobile application via the LinkBiz.Portal. These merchants include 124 utility and service companies, 186 educational institutions, 277 government agencies and local government units (LGUs), 140 cooperatives/associations/foundations/corporations, 20 hospitals/healthcare/clinics, and 16 banks, credit card companies and insurance companies. The OFBank’s approved conversion to digital bank is the first phase of the three-stage licensing framework of the BSP on the establishment of new digital banks.

LEARN MORE

Overseas Filipino Bank: The capstone of six years of financial momentum

(Written by Chris Wright May 30, 2022 | Published on Euromoney ) The Duterte presidency had many problems, but it gave the Philippine central bank and finance ministry room to enact significant change in tax, digital reach, infrastructure and fiscal policy. OF Bank will be among its legacies. The Philippines has long owed a debt to its overseas foreign workers (OFWs). Even after the disruptions of the pandemic, overseas workers sent back $31.4 billion to the country in 2021, and the central bank expects a 4% rise in that number this year. From Singapore to Saudi to a thousand merchant ships around the globe, these workers routinely send home sums equivalent to around 9% of the Philippines’ GDP. “Historically, OFWs have played a significant role in fuelling the country’s economic growth,” says Leila Martin, chief executive of Overseas Filipino Bank. “Now they are significantly contributing to our efforts to respond to the global health and economic crisis brought about by the Covid-19 pandemic.” OF Bank is a new institution – or more accurately an old one in a new form – which represents one of the signature missions of the now-ending regime of president Rodrigo Duterte: Financial inclusion. “We are trying … to make digital banking more accessible, more palatable to the appetite of Filipinos who traditionally are not very much into digital banking” - Leila Martin, Overseas Filipino Bank OF Bank was formed out of the Philippine Postal Savings Bank as a wholly owned subsidiary of Land Bank of the Philippines, which is a state institution historically focused on serving the needs of farmers and fishermen. With its transition, OF Bank becomes the first government digital-only branchless bank in the country, and has a mandate to provide financial products and services tailored to the needs of overseas Filipinos. And that is quite a need. OFWs have a more vital role to the Philippines than even the headline numbers would suggest, because pretty much all of those remittances – to parents, to spouses, to siblings, to kids – then go straight into productive use in the domestic economy. They are spent on food, housing, education and all the other things that domestic helpers, sailors and hospital workers around the world are sending money back to support. “These remittances elevate not only the financial conditions of their own families, but the financial position of the Philippines, spurring economic growth,” Martin says. Yet they are underserved in their offshore communities, sometimes cruelly so. People trying to send remittances home are stymied at every turn: draconian one-off fees, often applied to each remittance, so that someone trying to send a transfer apiece to mum, sister and daughter gets hit by the same fee three times. The list of hinderances continues: absurd foreign exchange rates; unrealistic minimums. In the first instance, OF Bank is about making this easier. Workers can access OF Bank through an app with a few pieces of ID and some links on their phones required for registration. There is no required opening deposit, no minimum balance requirement nor fear that an account will be closed for lack of funds coming in. There is 24/7 availability, no charges at all if transfers are between OF Bank accounts or to other Landbank accounts, and fees of P15 to P25 (between $0.29 and $0.47) to other commercial banks in the Philippines. Martin says the bank is not at this stage handling FX, but it has offered retail onshore dollar bonds issued by the Bureau of the Treasury, and there are plans to tie up with other partners who ought to be able to trigger reductions in conversion rates. Up and running About 18 months into its existence as OF Bank, most of the key services are up and running; there are 75,000 retail accounts on board, and in the three months to April there were P1.8 billion in banking inflows, P800 million from the remittances base. There is also a broader point about digital banking as a mechanism for financial inclusion, which has been a mainstay of Duterte policy, or rather a mainstay of Bangko Sentral ng Pilipinas governor Benjamin Diokno and Finance Secretary Carlos Dominguez under the broader poverty alleviation ideas of the president. “What we are trying to do at OF Bank is to make digital banking more accessible, more palatable to the appetite of Filipinos who traditionally are not very much into digital banking because of the apprehension that money will be lost because it’s in the air,” Martin says. “The pandemic jump-started the reduction in the digital divide.” This is certainly true: Diokno has said many times how the pandemic, as a mechanism for forcing digital engagement, accelerated state ambitions in this area by years. In this respect, OF Bank’s ownership is important. It is certainly not the only digital bank underway in the Philippines: Euromoney has written before about Tonik, for example, and there are digital platforms backed by Union Bank, RCBC, EastWest, CIMB and ING, among others. But OF Bank is owned by a state institution whose entire mandate is to stand for the 'little guy'.\ “There is definitely a stability in being a government bank,” says Martin. “It assures people that their hard-earned money is safe and secure. It also brings the resources of the parent: Martin, a specialist in electronic and internet banking as well as project management, is one of many who was seconded to Land Bank to build OF Bank. “I know that at Land Bank, our success rests largely on [the] strategic direction set by the seniors and the protocols that were established and proven to be effective,” she says. “And that is basically the blueprint for OF Bank transitioning.” It also places OF Bank squarely within the context of the Duterte administration’s ambitions as that reign comes to an end. “We fulfilled president Duterte’s promise of establishing a bank dedicated to the needs of Filipino workers working abroad… our first branchless digital-only bank in the country,” said Dominguez at an event in Manila in April. “It now serves overseas Filipinos in 116 countries.” Credit That conference felt like old times: The great and the good gathered in the Reception Hall, PICC Pasay City, to see presentations from the ministry of fnance and the central bank, not on a screen but in person. Duterte’s time was coming to an end – the new president, Ferdinand 'Bongbong' Marcos, formally takes o?ce on June 30 – and there was a sense of n de siècle about it all, a setting out of achievements and a call for continuity from the successors to come. It is an interesting and uncomfortable contradiction that while the Duterte regime has been lamentable in human rights and freedom of speech terms, it has been strikingly successful in terms of financial policy. Most people in financial services tend to lay the credit for this at the door of Diokno and Dominguez rather than the president, but he does deserve credit for leaving them to do what they are good at. It is quite a list. Diokno calls it “six years of institutionalized game-changing reforms and shaping the economy.” Dominguez claims: “Years from now, when we bring down poverty to single digits, we will look back at this time as when we made the turn.” Let’s take each in turn. From the BSP’s perspective, reform under the Duterte term began with the formation of the interest-rate corridor framework in 2016. In 2017 came the National Retail Payment system, allowing interoperability among payment service providers. Then came amendments to the BSP Charter in 2019, enabling the central bank to issue its own debt securities, providing it with an additional instrument for managing financial system liquidity. The Covid emergency prompted the Financial Institutions Strategic Transfer Act, or Fist, a pre-emptive strike against non-performing loans as the pandemic kicked in. In fact, Covid would give Diokno the ammunition he needed to make further sweeping changes. “The Covid-19 pandemic did not deter us from pursuing game changing reforms,” Diokno said at the Pasay City event. “In fact, the pandemic proved to be a catalyst that accelerated many of our reforms such as digitization and sustainability in our financial system.” This could be seen in action in two signature BSP initiatives. One is the Digital Payments Transformation Roadmap 2020-23. This has a target to convert half of the total volume of retail payments into digital form and onboard 70% of Filipino adults into the formal financial system using payment or transaction accounts by 2023. The other is the Digital Banking Framework, a key part of the DPTR, which granted digital bank licences to six financial institutions by the end of 2021. “The issuance of the Digital Banking Framework also aims to advance financial inclusion and the adoption and growth of digital financial services in the country,” Diokno says. Other initiatives include enabling regulations on Islamic banks, in order to attract funds from Islamic investors, and aiming to channel funds into infrastructure requirements in the Bangsamoro Autonomous Region in Muslim Mindanao. There has been the introduction of the basic deposit account framework; as of the second quarter of 2021, the number of basic deposit account holders in the country reached 7.4 million. Some 90.5 million Filipinos have basic and other types of deposit accounts. And the Sustainable Central Banking Programme and other sustainability and ESG frameworks have been launched. “The reforms that we have instituted are the result of our openness to embrace new things and our courage to deal with the challenges of our times,” Diokno said at the end of his presentation. “The past six years bested our resilience as a nation. But we are emerging better and stronger because we opted to build windmills that have harnessed the winds of opportunity. “When the winds of change blow, some people build walls. Others build windmills.” Policy pay-offs That’s the central bank. How about the government? In terms of policy, two things stand out: Duterte’s signature Build Build Build programme, and tax collection reform. Build Build Build committed to raise infrastructure spending to above 5% of GDP – it should reach 5.9% this year, according to finance secretary Dominguez. The difference is most visible in the railways. The government says the railway system covered just 77 kilometres before Duterte took office and now stands at 1,209km; the number of operational stations (61) has risen to 208; while the 224 operational cars of 2016 have become 1,368 today. All told, the department of finance has agreed 28 concessional loan agreements for its ?agship infrastructure projects, including the Metro Manila Subway project. That has been a long time coming: the Philippines is thought to be the world’s most populous city without a mass transit system, and Dominguez is particularly proud of that one. “What had once been considered a dream subway is now about to become a reality,” he says, adding that “our ?scal discipline” is what made it possible to agree the concessional loan arrangements that got it going. In truth, not as much infrastructure has been brought to operational status as the government would have hoped. But latitude has to be given for the disruption caused by the pandemic. The tax side involves the Comprehensive Tax Reform Programme, which lowered taxes, both personal and corporate, while simultaneously expanding the base, incentives and collection skills. Dominguez appears prouder of tax reform than anything else. “The administration decisively passed and implemented the most comprehensive tax reform programme ever in this country,” he said in his presentation. “This provided robust and recurring revenues that help expand social services and support our massive economic investments in modern infrastructure.” It is easy to illustrate the progress that has been made on tax. The government has doubled the annual collection it takes from government-owned or controlled corporations, an average of P68.7 billion annually since Duterte took office. Also 99.5% of income tax returns are now filed online, compared with just 10% in 2015. Overall tax revenue has increased from 15.1% in 2015 to 16.1% in 2019, before Covid kicked in. The government says the various elements of tax reform raised P504.6 billion in incremental revenues during the first four years of implementation. Two other important initiatives were the so-called sin taxes – more formally a number of excise taxes on sweetened beverages, from which the government collects P104 million a day now, to improve funding for its universal health care programme – and the Rice Tarification Law, which lowered rice prices and, the government says, provided a flow of funds for the modernization of the agriculture sector. Taxes on other suitably sinful items, such as alcohol, tobacco and vaping products, have gone up three times since Duterte took power. The rice law should not be glossed over: Dominguez notes that it took 30 years of failed attempts before it came into being, opening up the Philippine rice market and – Dominguez says –removing rice as a contributor to the main inflation rate and instead lowering the price of a vital staple food for 100 million Filipinos. That is a stark reversal in fiscal terms. Prior to the law passing in 2019, the National Food Authority received an average of P11 billion a year in tax subsidies from 2005 to 2018, the government says. It has instead earned P46.6 billion in rice-import tariffs during the first three years of the law’s implementation. “The rice tarification law ensures that farmers benefit directly by providing at least P10 billion each year for mechanization, high-quality seeds, access to credit and training,” Dominguez says. Three other things have worked in the finance secretary’s credit: the Ease of Doing Business Act; the Philippine Identification Act, which the Land Bank of the Philippines says has cleared the way for 7.7 million formerly unbanked registrants to be part of the formal banking system through implementing – 61.3 million individuals have registered for the national identity system as of March 23; and the revival of the Reit Act. The capitalization of the real estate investment trust sector was now P269.7 billion in April. OF Bank should be seen in the context of all of these reforms. Indeed, so should its parent: Dominguez says the government has infused more capital into the Land Bank of the Philippines (and Development Bank of the Philippines) than all other administrations put together. He wants to change its image. “Land Bank’s image as a big rural bank is far in the rearview mirror,” he says. “The robust capital infusion reinforced Land Bank’s financial strength and allowed it to be an effective partner of the government in advancing its development agenda. The capital is being prudently managed and used to finance projects that are needed by the country, not just in the agriculture sector,” including healthcare, education, power generation and distribution, water, transportation and housing, all led by the private sector. Covid costs There’s also room now to take a reckoning of the policies that were implemented in order to defend the country against Covid. Without question, the pandemic delayed progress. “Before Covid happened, the Philippines was in great shape: our debt-to-GDP ratio was only about 40%, our fiscal deficit to GDP was only about 3%,” says Alfred Dy, analyst at CLSA. “There was a lot of optimism. “But when Covid hit, the government had to step into the picture, to prop up the economy.” Debt to GDP has gone up to 60%, GDP has shrunk, and the fiscal deficit has risen to perhaps around 8%. “So, there’s some added leverage" says Dy, "but it’s something the government had to do.” The government argues that the impact of Covid would have been much worse without its measures. It was already bad – GDP fell 9.6% in 2020 – but would have been a 13.3% drop without reforms, Dominguez claims. All told, the government spent P3 trillion in direct response to Covid, equivalent to 15.6% of GDP, and ?nanced it by prioritizing domestic borrowings as well as seeking o?cial development assistance, and then the international capital markets. Vaccines were financed through a joint arrangement with the World Bank, the Asia Development Bank and the Asia Infrastructure Investment Bank. Now, some of those measures are being unwound. The government’s provisional advance arrangements with the central bank stood at P540 billion at its peak, now P300 billion, and will be paid o? by June 12, Dominguez says. Initial fears for the health of the banking sector so far appear overdone – although nobody is out of the woods yet, and the Fist Act, which for a while seemed a useful backstop that wasn’t going to be needed, may yet prove essential. “Because of the Covid crisis, you’ve seen non-performing loans moving up a bit,” Dy says. "But clearly what you’re seeing now can’t be compared to what we saw in the 1990s with the Asian financial crisis." “Because of the Covid crisis, you’ve seen non-performing loans moving up a bit,” Dy says. "But clearly what you’re seeing now can’t be compared to what we saw in the 1990s with the Asian ?nancial crisis." Then, system NPLs went as high as 20%; today they stand at 4.5%, and among the bigger banks that CLSA covers, below 3%. “The banks are well-capitalized, and the feeling on the ground is that if we are at 4.5% NPLs, that is quite good. We don’t see any systemic risk,” says Dy. CLSA is forecasting 7% to 8% loan growth this year, up from 4% to 5% last year. The Philippines underwent a multi-year push to hit investment-grade and its status has not yet been threatened by the pandemic. In February, Fitch a?rmed the Philippines as BBB, albeit with a negative outlook, citing strong external bu?ers and growth but weaker structural indicators including per capita income and governance. “The negative outlook reflects uncertainty about medium-term growth prospects as well as possible challenges in unwinding the policy response to the health crisis and bringing government debt on a firm downward path,” the agency says. It forecasts a recovery from 5.6% GDP growth in 2021 to 6.9% in 2022 and 7% in 2023. At Moody’s, Joyce Ong maintains a stable outlook for the Philippines banking system. “The accelerating in?ation due to the Russia-Ukraine military conclict, lingering pandemic woes due to new variants, and possible rate hikes in the country will dampen but not derail the economy’s recovery,” she says. She expects bank profitability to improve as provisions decrease and core earnings pick up. She also thinks banks recognized most of the defaults by pandemic-hit small and medium-sized enterprises and retail borrowers in 2021, and therefore expects NPL growth to slow through 2022. In the aggregate, Diokno and Dominguez can look back on their work under Duterte with some satisfaction. And when it looks back years from now, perhaps OF Bank will be among the signature achievements of the period: Finally giving a hard-working and essential part of the Philippine national identity the Financial services they deserve. “We want to further our portfolio,” says Martin, “with an ear to what the requirements are of our overseas Filipinos.”

LEARN MORE

OFBank supports 18-Day Campaign to End VAW 2024

Nakikiisa ang OFBank sa 18-Day Campaign to End Violence Against Women (VAW) ngayong ika-25 ng Nobyembre hanggang ika-12 ng Disyembre 2024. Sa temang “UNiTEd for a VAW-free Philippines" at sub-theme na “VAW Bigyang Wakas, Ngayon na ang Oras", binibigyang-diin natin ang kahalagahan ng sama-samang pagkilos para sa mas ligtas at pantay na kinabukasan ng mga kababaihan, kasabay ng ika-20 anibersaryo ng paglagda sa Republic Act No. 9262 o ang "Anti-VAWC Act of 2004." OFBayanis, sabay-sabay nating itaguyod ang isang VAW-free na mundo!

LEARN MORE

OFBank joins DMW Mega Jobs Fair to support overseas Pinoys

MANILA, Philippines — In celebration of the 123rd Labor Day, the Overseas Filipino Bank (OFBank) participated in the Mega Jobs Fair for Overseas Employment hosted by the Department of Migrant Workers (DMW) at Robinsons Galleria, which attracted thousands of job seekers aspiring to secure employment opportunities abroad. The event served as a key platform for OFBank to connect with aspiring Overseas Filipino Workers (OFWs) and introduce its comprehensive suite of digital banking solutions — designed to safeguard their hard-earned income and minimize remittance costs. OFBank President and CEO Elcid Pangilinan emphasized the digital Bank’s commitment to protecting the financial interests of migrant workers and their families. "Tumutulong kami na mapaabot ang tulong sa mga pamilya at beneficiaries sa isang ligtas na paraan at sa maliit na cost," said Pangilinan, highlighting the importance of accessible and reliable banking services tailored to the unique needs of Filipinos working overseas. DMW Secretary Hans Leo Cacdac also expressed gratitude to OFBank's continuing partnership and support for Overseas Filipinos. Throughout the Mega Jobs Fair, OFBank engaged with potential clients by providing information on its full range of offerings, including remittance solutions, savings accounts, and investment opportunities — all accessible through the OFBank Mobile Banking App (MBA). OFBank's participation in the event underscores its ongoing commitment to supporting overseas Filipino communities and enhancing their financial well-being. As the country’s first branchless, digital-only bank dedicated to overseas Filipinos and their beneficiaries, the Bank reaffirms its role as a trusted partner of Overseas Filipinos, ensuring their financial security and success.

LEARN MORE

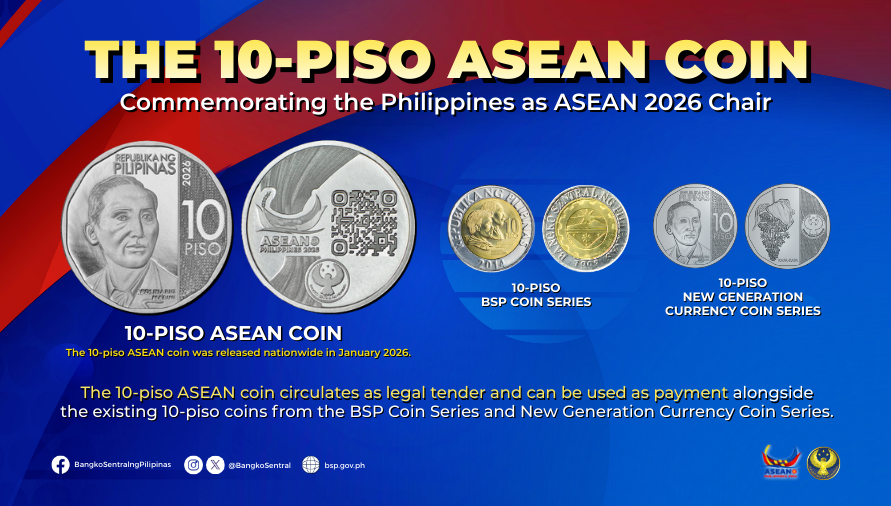

10-piso ASEAN 2026 Coin

The BSP-issued 10‑piso ASEAN Coin can now be used as legal tender for everyday transactions, alongside existing 10‑piso coins. This commemorative coin marks the Philippines’ role as ASEAN 2026 Chair, highlighting regional cooperation and shared goals among ASEAN Member States.

LEARN MORE

OFBank cuts transfer costs to help overseas Filipinos maximize every peso sent home

Sending financial support to families back home is now more affordable for Filipinos abroad. The Overseas Filipino Bank (OFBank), LANDBANK’s wholly-owned digital banking subsidiary, is removing transaction fees for all InstaPay transfers made through the OFBank Mobile Banking App (MBA) starting July 7, 2026. With this, OFBank account holders can transfer funds to other local banks and e-wallets free of charge, ensuring more of their hard-earned money goes directly to their families. The move mirrors LANDBANK’s simultaneous rollout of a comprehensive zero-fee framework, supporting the directive of LANDBANK Chairman and Finance Secretary Frederick D. Go to accelerate digital financial inclusion by making banking services more affordable and efficient for Filipinos. “By extending our zero-fee digital banking ecosystem to OFBank, we are ensuring that the same benefits uplifting our workers and small business owners at home now reach Filipinos overseas. Removing fund transfer fees helps our overseas kababayans maximize the value of every peso they send home, making it easier to provide vital financial support to their loved ones without the burden of extra costs,” said OFBank Chair and LANDBANK President and CEO Lynette V. Ortiz. The initiative also complements OFBank's participation in LANDBANK's zero-fees person-to-government (P2G) payment program, which waives convenience fees for eligible government payments made via QR Ph until December 31, 2026. Through this program, OFWs, Overseas Filipinos, and their families can manage both personal finances and national or local government dues from a single account without incurring additional charges. “As a banking partner of our kababayans abroad, OFBank continues to make digital banking more responsive to their needs. Through this initiative, we give our clients greater flexibility to send support to their families back home,” said OFBank President and CEO Leila C. Martin. These efforts are in line with President Ferdinand R. Marcos Jr.’s directive to strengthen digital financial services and expand access to efficient, affordable, and accessible banking services for all Filipinos. Likewise, it is aligned with Bangko Sentral ng Pilipinas (BSP) Circular No. 1238, Series of 2026.

LEARN MORE